REINZ Chief Executive Jen Baird says that the market is subdued, despite nationally seeing higher sales counts, properties selling more quickly, increased stock levels, and more listings, compared to a year ago. These increases are a contrast with the much lower measures seen in April 2023, following the impacts of weather events like cyclones Hale and Gabrielle, but are below the average for this time of year longer-term.

The total number of properties sold in New Zealand decreased by 17.3% compared to March 2024, from 6,721 to 5,559, and increased by 25.3% year-on-year, from 4,438 to 5,559. All but one region saw increased year-on-year sales activity, the exception being West Coast, where sales decreased by 5.3% compared with April 2023. “Sales activity lifted in 15 of 16 regions, compared with April 2023. Ten of those regions recorded increases of over 20%, with Marlborough (45.8%) recording the highest year-on-year lift in sales. The April 2024 sales figures reflect greater demand, after the impacts of weather events in early 2023. However, sales figures are still below long-term averages in many regions." says Baird.

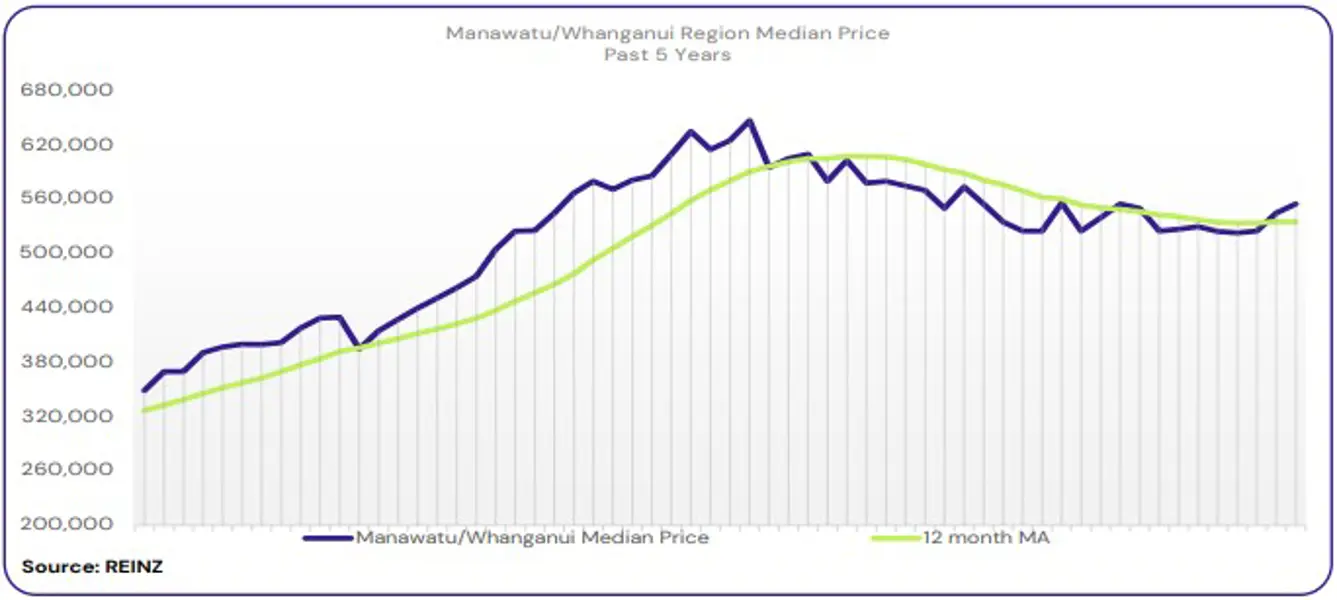

Nationally, median Days to Sell decreased by 3 days, from 46 to 43 days, compared to a year ago. For NZ, excluding Auckland, median Days to Sell decreased by 7 days year-on-year, from 48 to 41 days. In 13 of 16 regions, median Days to Sell were lower compared with April 2023. The biggest decreases were in Tasman (down 29 days), Marlborough (down 18 days), Northland (down 17 days), and Wellington (down 11 days). In contrast, some regions recorded the highest median days to sell for several years: Auckland had the highest days to sell in the month of April since 2001, Manawatu-Whanganui since 2015, and West Coast since 2019.

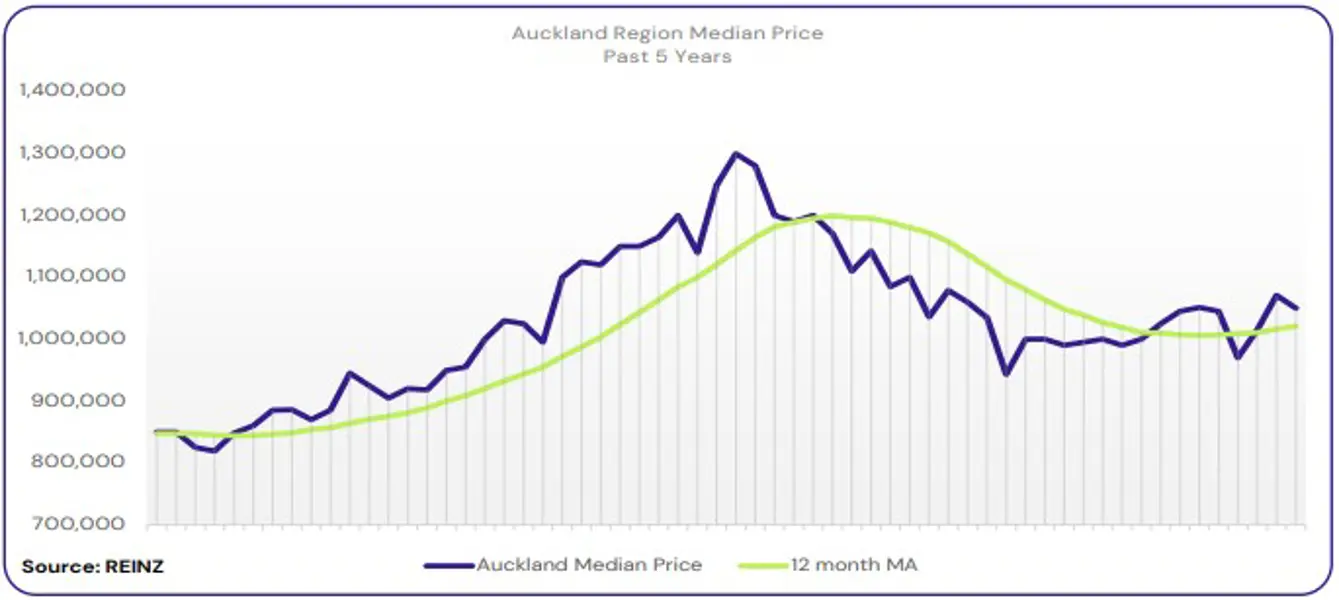

The national median sale price increased by 1.3% year-on-year, from $780,000 to $790,000, and decreased by 1.3% compared with March 2024, from $800,000 to $790,000. For NZ excluding Auckland, the median price of $700,000 was the same as for April 2023; month-on-month, it decreased by 1.7%, from $712,000 to $700,000.

“The median national sale price has now increased year-on-year for the third consecutive month, and sales are picking up as well. There are vendors who will need to sell and don’t want to wait any more, and these vendors will need to set realistic expectations, both for price and the time needed to sell their property. The median price for NZ excluding Auckland hasn’t changed compared with April 2023. This may suggest that, with more properties to choose from, some buyers have less competition from other buyers, and some are more comfortable taking a stronger approach to their negotiation,” she says.

While the April data shows more activity in the housing market, with year-on-year increases in sales, listings, stock levels, and median prices, it’s clear that economic factors are creating headwinds. “Activity is picking up for the housing market as we move into autumn, with sales lifting and more choices for buyers. However, the likelihood of interest rates staying at these elevated levels for a while, and more talk of job losses, continues to lead to caution among some buyers.

There seems to be plenty of buyer interest, with many seeing the current price levels as attractive, but some are taking their time before making a decision. Similarly, some vendors are selling now and are open to meeting the market with their pricing, while others prefer to wait. Nationally, prices are still below their peaks from a few years ago and sales are still lower than long-term averages. Although the cooler months traditionally lead to activity slowing down, demand for properties may increase as investors return to the market in response to upcoming changes to the bright line test and the reintroduction of interest deductibility on investment properties. With this in mind, buyers may want to act now,” adds Baird.

Regional highlights

- In 15 of 16 regions, the year-on-year sales count was higher, and 10 of those regions increased by over 20%. Marlborough recorded the greatest increase in year-on-year sales count, up by 45.8%.

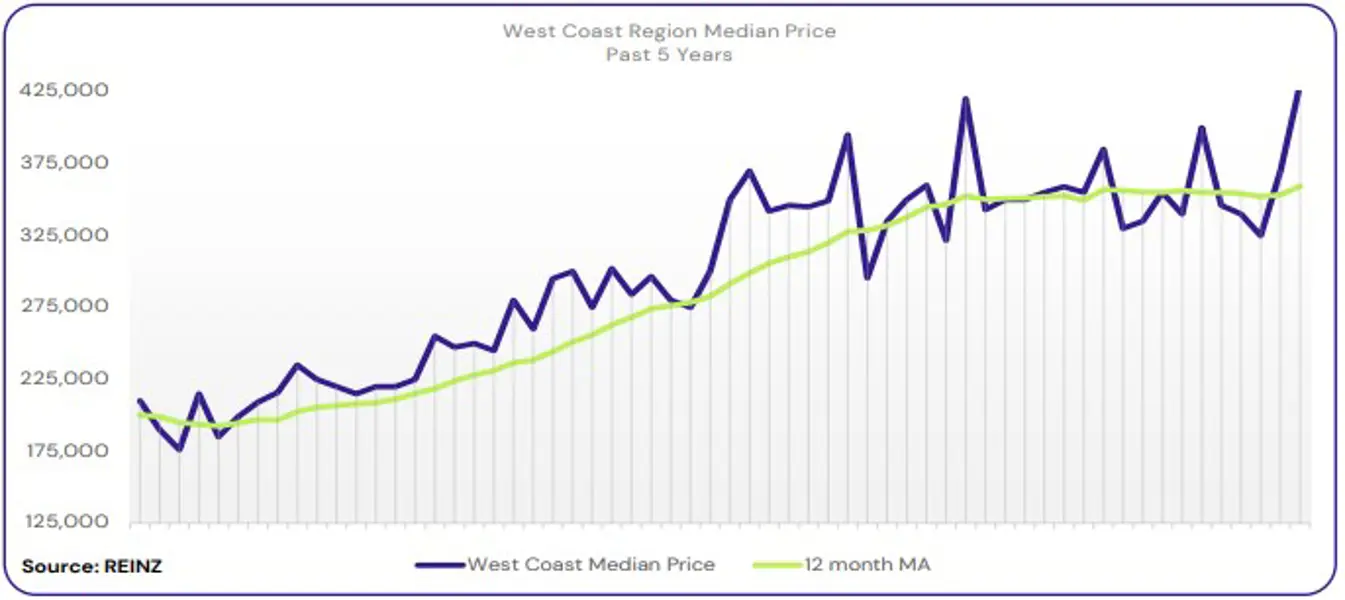

- 10 of 16 regions had year-on-year price increases. West Coast had the greatest increase, up by 19.8% compared with April 2023.

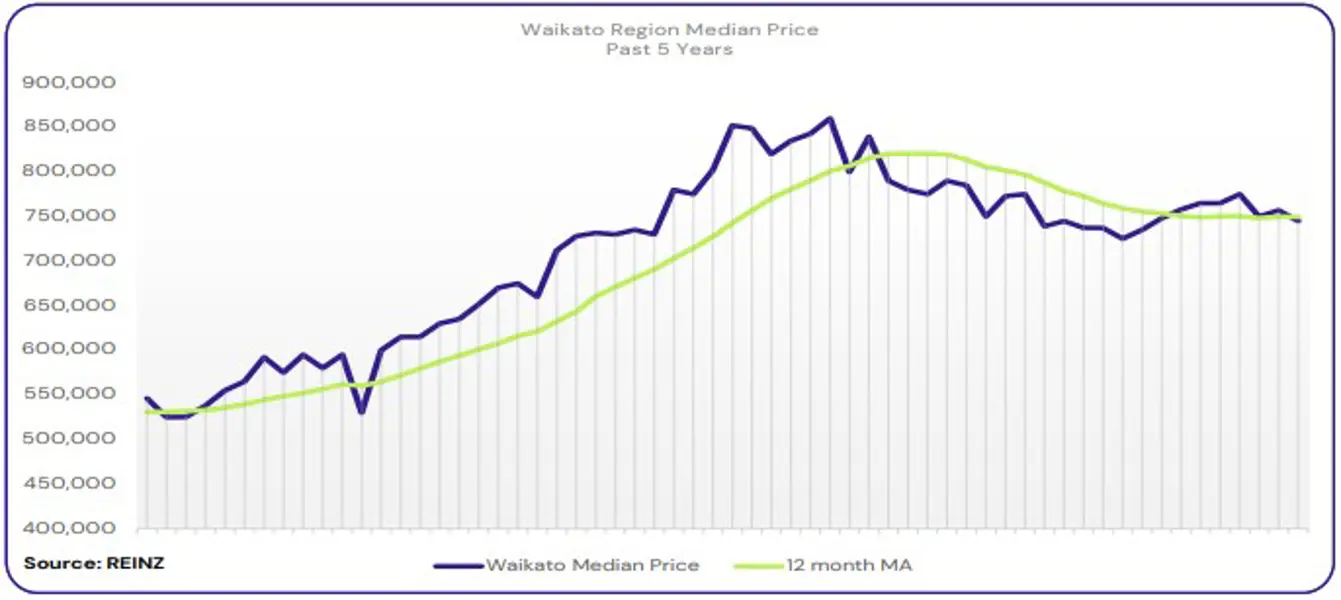

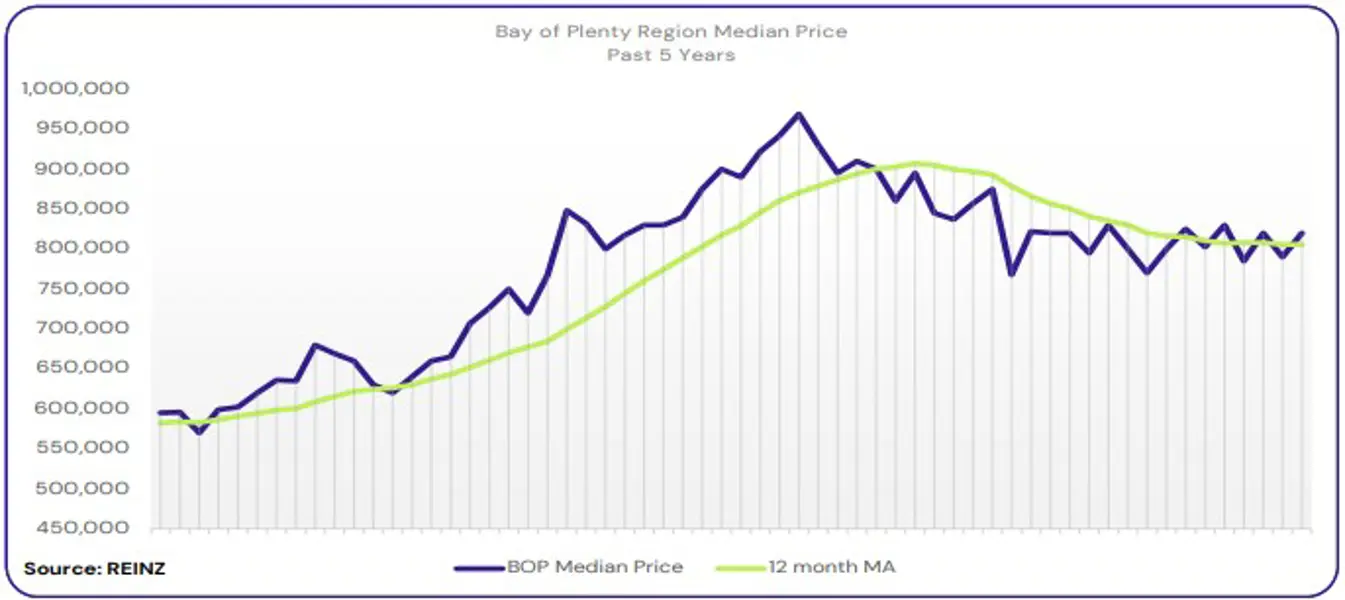

- 13 of 15 regions saw year-on-year increases in new listings, with nine of those regions recording increases of over 25%. Wellington had the biggest increase, up by 318 listings year-on-year (69.0%). Other notable increases in listings were Auckland by 1,034 listings (41.1%), Waikato by 209 (36.8%), Bay of Plenty by 179 (39.7%), Manawatu-Whanganui by 93 (29.8%), Taranaki by 65 (39.6%), Marlborough by 35 (46.1%), Canterbury by 337 (32.5%), and Otago by 107 (55.2%).

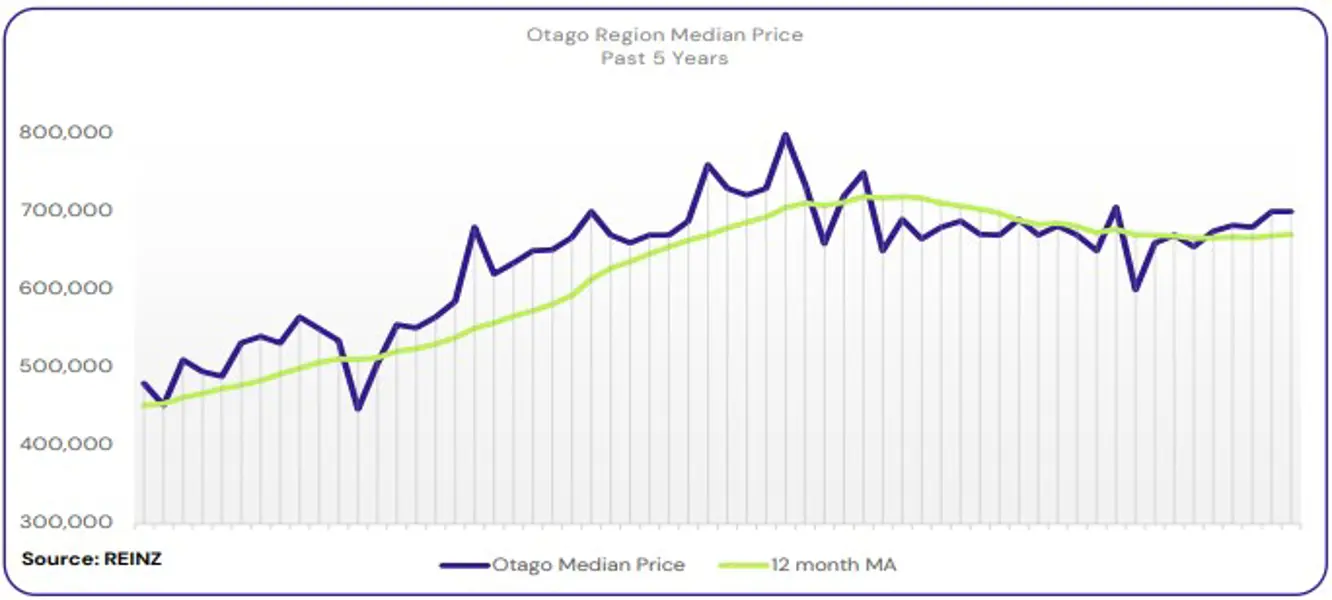

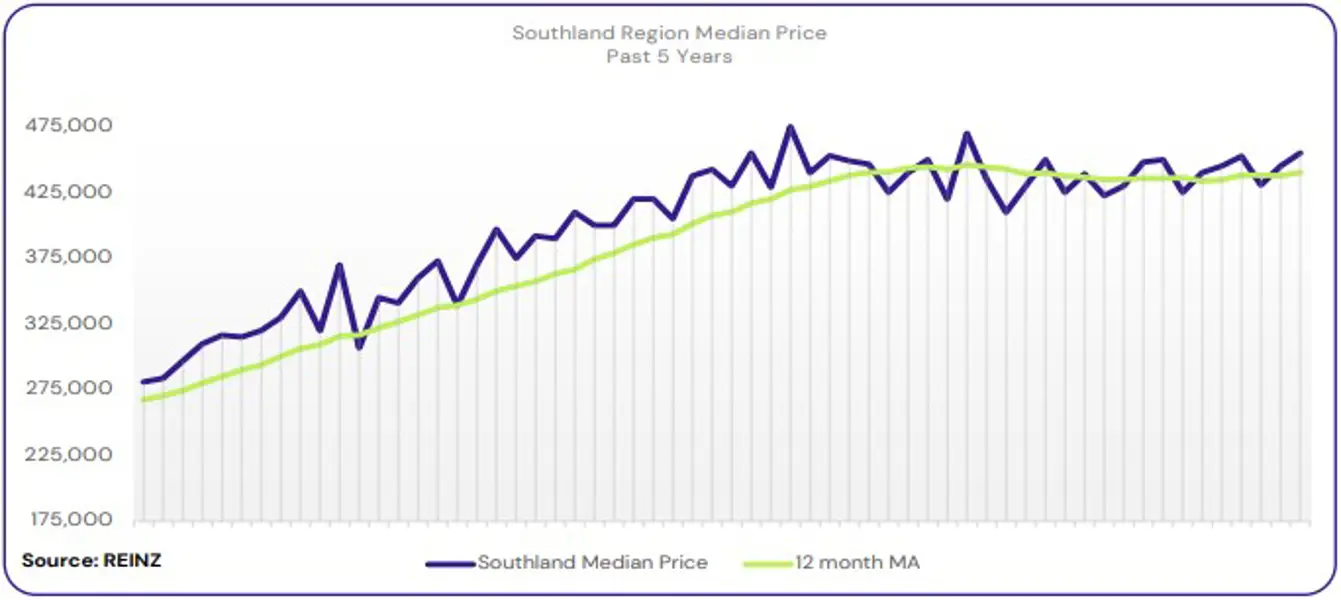

- Southland is the top-ranked region for HPI year-on-year movement this month. Otago is second and Bay of Plenty is third.

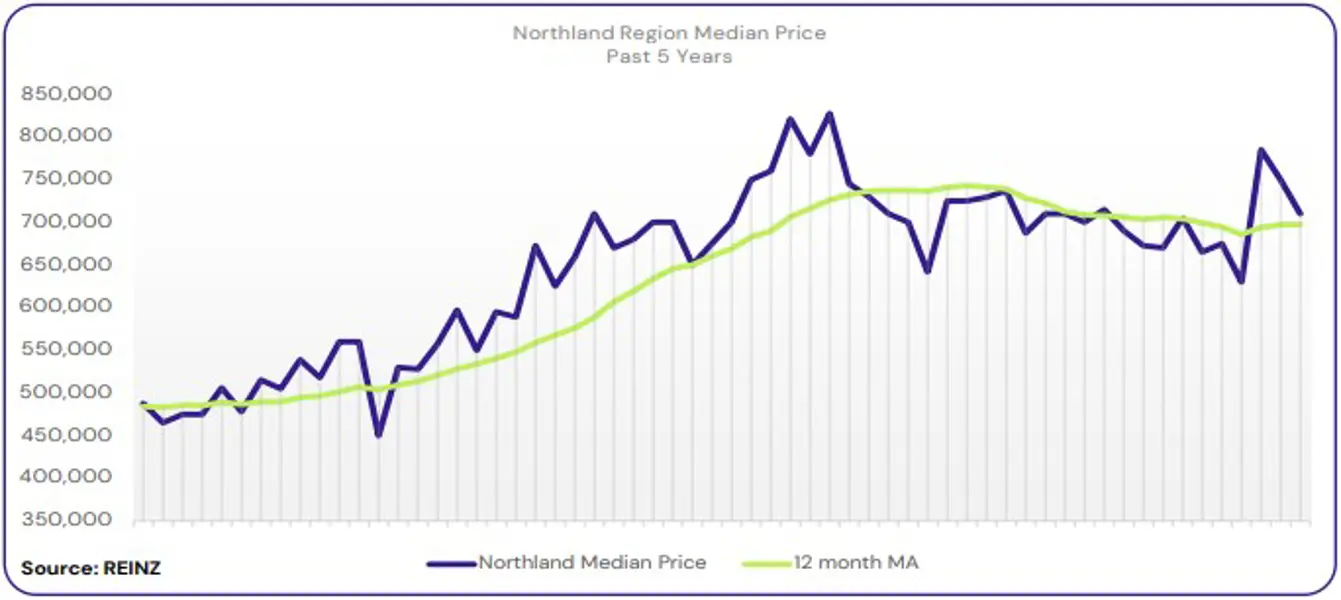

Regional Analysis - Northland

The median price for Northland decreased 1.4% year-on-year to $690,000.

“Local agents report that first-home buyers and owner occupiers remained the prominent buyer groups across the region. Investors and developer enquiries are also increasing in Whangarei.

Most vendors are willing to meet the market’s expectations, while some are taking longer to adjust. Open home attendance was variable, with the lower-priced listings seeing a lot of activity.

The number of auctions increased compared to this time last year, but sales through this method remained light. Local agents predict that activity will remain consistent but could shift later in the year depending on how investors react to upcoming policy changes.” (REINZ)

The current median Days to Sell of 56 days is more than the 10-year average for April which is 51 days. There were 53 weeks of inventory in April 2024 which is 13 weeks more than the same time last year.